Market Correction in Alternatives/ Real Estate

- socialmediaemaildz

- Sep 16, 2021

- 7 min read

Recent Discussions

The elephant is in the room again. Recent worries about a higher inflation in the Euro zone have triggered a discussion about the European Central Bank to exit its expansive monetary policy which was initially implemented as a bail-out program during the financial crisis as well as during the Covid19 - pandemics.

Though, given the current stage it is feared that solely reversing the bail-out programs will not be enough. Instead, the renunciation of the zero interest rate policy accompanied with a distinct rise in reference rates might be necessary to extinguish the flamelet of a burgeoning higher inflation rate.

Provided this, capital intensive industries like the real estate investment business could get harmed because cheap money as one of the drivers of current all-time-high market prices in a lot of asset classes and regions might be not so cheap anymore.

In short (and a bit simplified), higher inflation as trigger for higher reference rates causes investment funding to dry up and prompting real estate prices to slump.

Dropping asset prices will further move investors to seek the market exit, triggering another wave of falling market prices — and off it goes: another real estate market bubble finally bursts.

In summary, the consequences for the European real estate markets may be severe. Or — it is just another crash scenario “prophecy” never being close to materialise.

Inflation, reference rates and the real estate market

Dr. Jörg Krämer/ Chief Economist of Commerzbank revealed his thoughts on this topic in a recent LinkedIn — post:

Real estate bubble in the Euro zone? The perspective of a long period of time without considerable yields pushes investors into tangible assets like real estate. In the first quarter (of the year 2021), real estate prices in the Euro zone rised by almost 6% compared to the previous period of time. As from the launch of the EURO in the year 1999 housing prices increased by approximately 40% more than rent levels did. Given this, real estate is more expensive than they were before the burst of the real estate bubble in the year 2008. This is especially true for some Euro zone core countries like France or Belgium.

A high valuation alone does not set off a crisis in the real estate market. This does not go without any trigger — e.g. considerably rising interest rates. But this can be the issue in a few years, in case rising inflation rates force the European Central Bank to set higher reference rates. In order to reduce the danger of a real estate market bubble already in an early stage, European Central Bank should start to counteract and exit the expansive monetary policy. — Quote end.

Well, when financing gets more expensive then there is little doubt that this will have certain impact on funding structures, investment volumes and eventually asset prices in the real estate market.

Question is, are we talking about a maybe overdue correction of markets? After all, those markets have been booming as from the end of the last big financial crisis.

Or, are we talking about the (pricing) air going out of a market bubble in a very destructive way?

Real estate investment yield levels in many of the real estate markets in the Euro zone are on a historic low which raises investment challenges in itself.

On the one hand, lower yields mean higher market prices. But at those low levels, market prices really jump and put much higher requirements on the equity and debt financing volume.

While higher debt financing ratios shall support the generation of satisfactory equity yields, the rent income levels of those assets find their limits in providing a necessary debt service capability.

This is exactly the situation, “cheap money” jumps in and provides a cushion, i.e. allowing for higher debt leverage without endangering the liquidity situation of a project or a company — at least for the moment.

Here, as an example is the outlook of an office investment based on an investment yield of 3 % p.a. on a 5 years investment term with a debt funding of 85 % on annuity repayment schedule, simulated based on the current dynamics of the respective market.

A 13 % p.a. equity yield is still expected. Though, simulation reveals an almost 50 % risk of overall loss with the investment (see the red zone in the graph Equity Yield Risk).

On the other hand, in terms of current liquidity (see graph Overall Funds from Operating) the chances of falling short of cash during the investment term is just 10% (see red zone) despite the high debt leverage.

The debt service capability (see graph DSCR Default Risk for Senior Loan) has an expected rate of around 1.08 — not thrilling though not bad at all for this debt ratio.

The situation immediately changes when the reference rate is increased by just 100 bps.

No words needed. I would say.

At this leverage, the risk of an overall loss moves from just under 50 % to almost 65 %. The project is short of current liquidity and the debt service for the loan is by far not sufficient anymore.

In short, there is immediate need for adjustment.

The negative impact of higher interest rates on the risk profile of a project is obvious and does not come with big surprises.

If this is enough to send a market into the abyss or if this is the trigger for some minor to mid-range market correction is not so clear and will -in may point of view- also depend on other factors, e.g. alternate investment opportunities, general market sentiment, refinancing possibilities especially with respect to corporate bonds and similar.

Investment Yield Level - one of those "other" factors

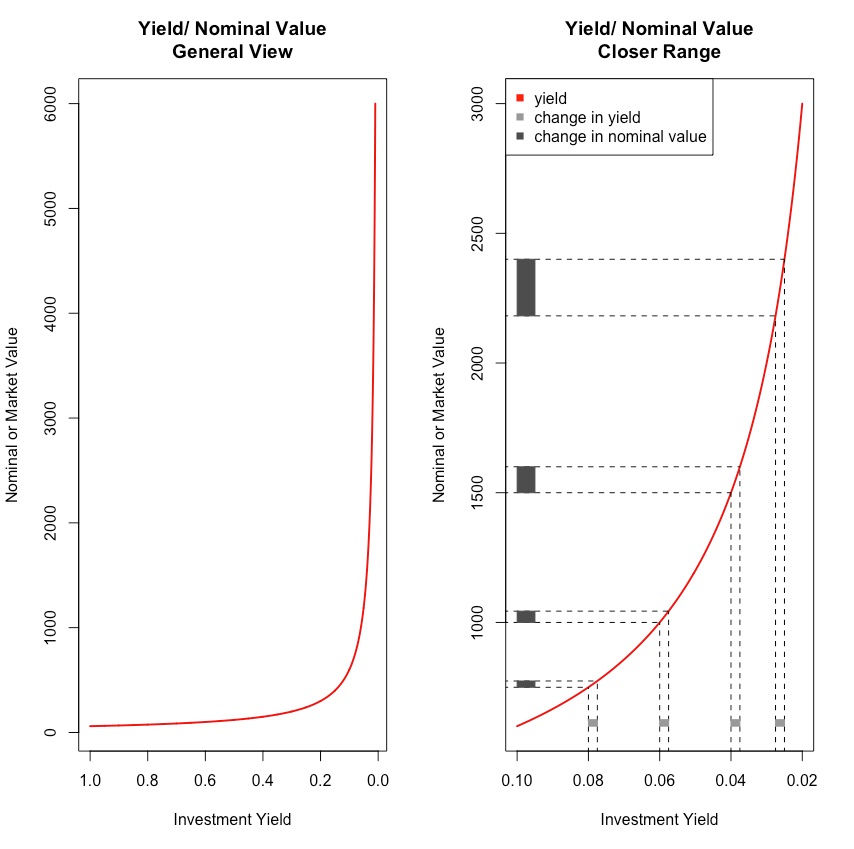

I already mentioned before that investment yields are at very low levels.

The problem — at current yield levels, nominal market valuations show a far more erratic behaviour already within small yield changes than this would be the case at a bit higher yield levels.

The following graph shows this quite well. The impact of the same change in yield gets exponentially higher the lower the yield level is.

Putting this notion forward, market values are quite influential with respect to Net Asset Values (NAV) of real estate companies (NAV was meanwhile replaced by Net Tangible Assets or Net Reinstatement Values according to newer EPRA definition which is in general the same for the purpose of this article).

So, small changes have a much heftier impact on the balance sheet of real estate companies in general and Net Asset Values in particular.

We take a short example to make this point more obvious. A real estate company faces the following balance sheet situation:

Real estate assets are valued at a yield of 7 % p.a.

When the investment yield changes from 7 % p.a to 7.25 % p.a., i.e. a mere 25 bps increase, there is not so much change in the overall framework:

While taking the current income and latent tax effects into account, the Net Asset Value decreased by just 2 %.

Now, we take the same framework with respect to rent income and debt ratio but the assets are valued at 3 % p.a. Balance sheet of the company as follows:

Again, there is this slight increase in the investment yield from 3 % p.a. to 3.25 % p.a.

The Net Asset Value in this scenario (and including running income as well as latent tax effects) decreasesby 12 %!

In case of a e.g. 50 bps increase of the respective investment yields, the net asset value decreases by 7.5 % compared to 23 % in the lower yield level scenario.

Once more, this is a huge difference but as said before, the impact caused by small changes is much higher on those lower investment yield levels. And this is exactly what we currently face in many real estate markets.

Those scenarios seem even more relatable when breaking it down to a metrics like NAV per share.

Apart from other things, NAV/share is often used for comparing current share prices with the inherent value of a company. In take-over bids the NAV/share is frequently used to argue in favour or against the take-over offer.

Imagine a take-over bid of e.g. EURO 42, — per share while the current NAV per share amounts to EURO 44, — . Given those circumstances, a 12 % decrease of the NAV by a slight hickup of the market is already a more dramatic event and might change circumstances very quickly.

Nevertheless, erratic changes in Net Asset Values as an isolated event might trigger stock exchange reactions but might not be strong enough to trigger any drastic deteriorations in a real estate market.

Though, it is definitely a piece in the puzzle when contemplating possible unfavourable market reactions.

Apart from this, the short-term nature of price settings in the stock market compared to the mid- to long-term price developments in a real estate market showed that the reaction in the stock market settles in much faster when an upcoming crisis is maybe still less obvious in the real estate market itself.

Here is an overview of some share price developments when the last financial crisis started to sneak in. Share prices reacted first, then the overall market followed.

Conclusion

In my point of view, the risk of higher inflation rates and a reaction by the European Central Bank is to be incorporated in the risk consideration of real estate companies.

The risk of funding to get more expensive is definitely in — with all its consequences.

If things go so far to end up in a disruptive market correction will not depend on one single topic, but rather on the evolving of several different issues in parallel (partly dependent on each other) which will influence the real estate markets unfavourably and with growing momentum.

Some of those topics I discussed in this article.

Though instead of musing and speculating about future market developments, the job of a strategic risk management is to identify those risk triggers, weight and quantify them in their isolated appearance as well as in their interaction with other risk triggers and evaluate the risk bearing capabilities of the own venture.

As a result, adjustment in one own’s risk position and, if necessary, de-risking of market exposures are to be executed in order to prepare for maybe rougher times.

By the way, this “maybe” is quantified in terms of probability and has therefore a clear “price ticker”.

Comments